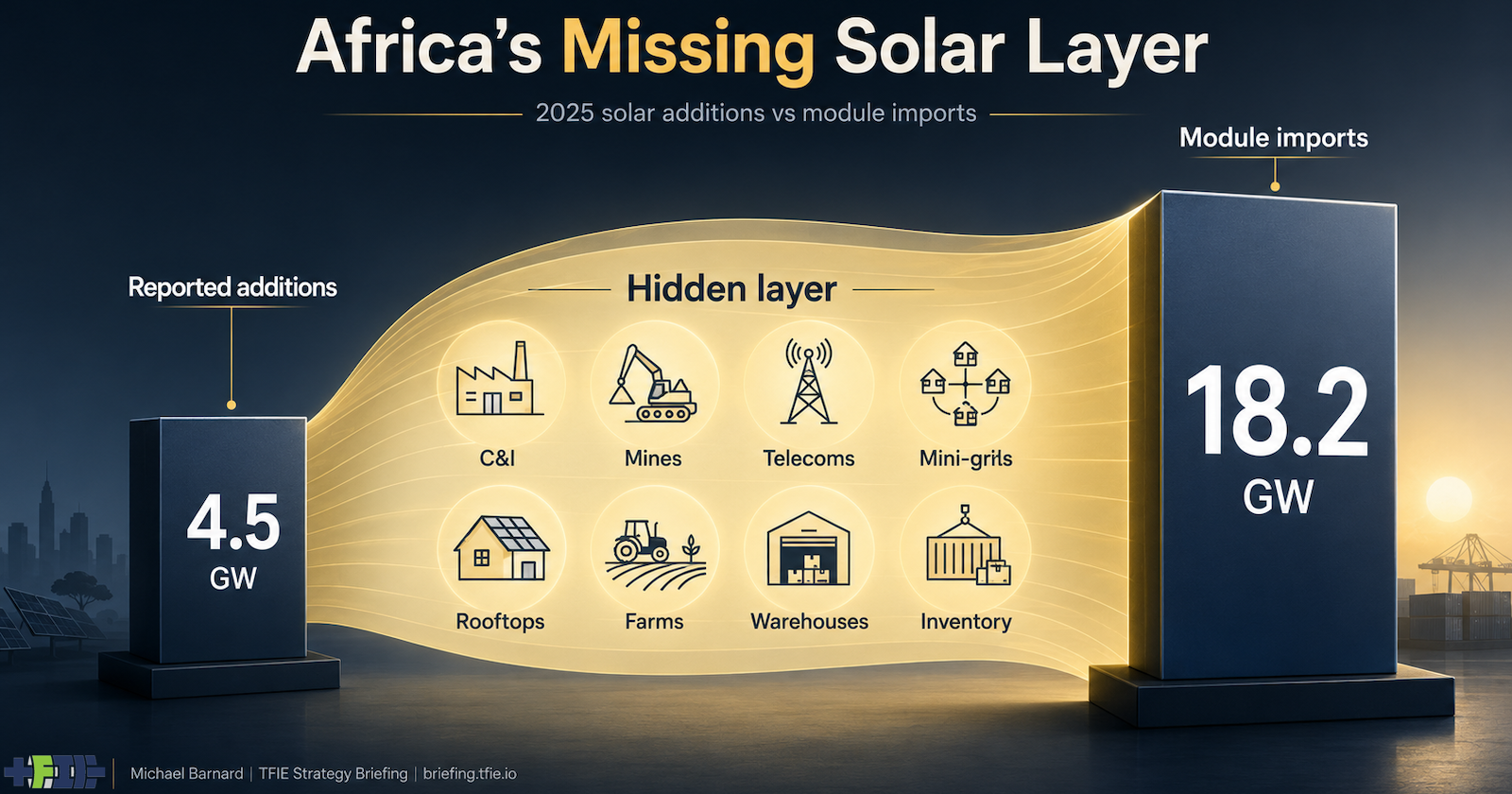

Africa's solar revolution may be moving far faster than official statistics suggest. While the continent reported installing 4.5 gigawatts of solar photovoltaic capacity in 2025—a respectable 54% year-over-year increase—a striking gap has emerged in the import data that tells a more dramatic story: African countries imported 18.2 gigawatts of solar modules that same year. The mismatch between what was officially commissioned and what physically arrived at African ports and warehouses reveals a hidden energy transition unfolding behind the scenes.

This gap matters because it reflects the difference between visible energy infrastructure and real-world electrification. Official statistics capture grid-connected utility projects with government announcements and ribbon-cutting ceremonies. They are far less effective at tracking what procurement managers, mine operators, telecommunications firms, farmers, and households are actually doing: buying solar panels to reduce dependence on weak grids, expensive diesel, and unreliable fuel trucks. When a clinic installs panels to power its lights and refrigeration, or a telecom tower deploys solar to cut fuel costs, or a farmer pumps water with solar energy, these systems often languish in warehouse inventory counts rather than official deployment figures—especially when they operate off-grid or behind meters.

The physical reality of those 18.2 gigawatts arriving in containers tells a different story than the formal 4.5 gigawatt installation count. Some modules are indeed waiting in warehouses—delayed by financing gaps, missing inverters, or a shortage of skilled installers. Others may be destined for projects not yet commissioned, or re-exported to neighboring markets. But the scale of the discrepancy is too large to dismiss as mere bureaucratic lag. A gap of 13.7 gigawatts represents real hardware, sitting in real places, waiting to be bolted onto roofs, fields, mining operations, telecom sites, clinics, schools, and mini-grid systems across the continent.

Africa's clean-energy transition is being propelled by a reinforcing set of conditions: Chinese solar modules continue flooding into African markets at plummeting prices, while batteries grow cheaper by the year. African grids remain weak, incomplete, or unreliable in many countries. Diesel remains expensive. And critically, the continent's improving logistics networks—Chinese-built ports, roads, rail corridors, and cross-border trade frameworks under the African Continental Free Trade Area—are making it easier for hardware to reach customers inland. These pieces fit together in ways most observers outside the continent have barely noticed.

The contrast with India is instructive. India installed 36.6 gigawatts of solar in 2025, the vast majority through large-scale utility projects captured in formal national auctions and grid connection agreements. India has a unified national market with mature reporting machinery that can see most of what happens. Africa is not a country; it is dozens of markets with different grids, policies, currencies, and political economies. This fragmentation makes distributed solar—installed by businesses and households, not governments—much harder to count but potentially much faster to deploy.

The headline projection circulating is that Africa might install 20 gigawatts of solar in 2026. Official new installations jumping from 4.5 to 20 gigawatts in one year would be extraordinary. But if the 18.2 gigawatts of imported modules in 2025 represent pipeline inventory now activating, and if distributed solar keeps flowing through informal and off-grid channels, the real installed base could be growing far faster than official numbers reveal. The continent's energy transition may not announce itself with government ceremonies. It may arrive quietly, in containers, deployed by farmers, miners, clinics, and households tired of waiting.