The European Union is engineering a elegant solution to a stubborn climate problem: using the automotive industry's vast purchasing power to kickstart a green steel revolution across the continent. The mechanism at the centre of this strategy is deceptively simple—low-carbon steel credits embedded in the EU's vehicle CO₂ standards—but its ambitions are sweeping: to create an entire lead market for fossil-free steel production that transforms Europe's industrial base while cutting the carbon footprint of every car rolling off assembly lines.

Steel is the skeleton of every vehicle, and the automotive sector's demand is enormous. Right now, most of that steel is produced the old-fashioned way, with significant carbon emissions baked into every tonne. But what if carmakers were rewarded—through CO₂ credits—for switching to genuinely clean steel? The economics suddenly shift. Investors see a real market emerging. Steel manufacturers commit capital to new, zero-emission production methods. And Europe's industrial advantage deepens.

The challenge, as transport and environment advocates at T&E have documented, is ensuring the credits actually deliver climate benefits rather than become a shell game of accounting tricks. Their recommendations are precise and uncompromising. From 2035 onwards, only fossil-free primary steel should qualify for credits. Any credit scheme that rewards weaker or transitional pathways beyond that date would send the wrong signal to investors, undermining the entire point of the mechanism. The EU Commission must also move quickly, adopting a clear methodology to define "low-carbon" steel by the end of 2026. Without regulatory certainty, carmakers and steelmakers cannot plan investments confidently.

The structure matters just as much as the definition. T&E proposes a limited transition phase starting in 2030, rewarding early movers who commit to genuine decarbonisation—but with strict conditions. Credits should be capped at 3% of carmakers' CO₂ targets from 2030 to 2034, keeping the mechanism focused and preventing gaming. Critically, this credit system should stand alone, freed from competing flexibilities that would dilute demand for green steel. If carmakers can meet their targets through cheaper fuel switching, they will, leaving green steel investment stranded.

Primary steel production should be prioritised, though paired carefully with recycled material. A dynamic baseline that accounts for scrap content is essential—it captures real emission savings in primary steelmaking while blocking windfall credits from simply using more post-consumer scrap without genuinely lowering emissions. T&E proposes that only post-consumer scrap should count toward the credit calculation, ensuring the signal remains true.

Perhaps most importantly, the lead market must stay anchored in Europe. Only EU-made green steel should qualify for the full credit benefit, with limited imports of green iron allowed from 2035 onwards—capped at no more than 50% of eligible steel. This keeps the industrial prize at home, strengthening European manufacturers and the workers they employ.

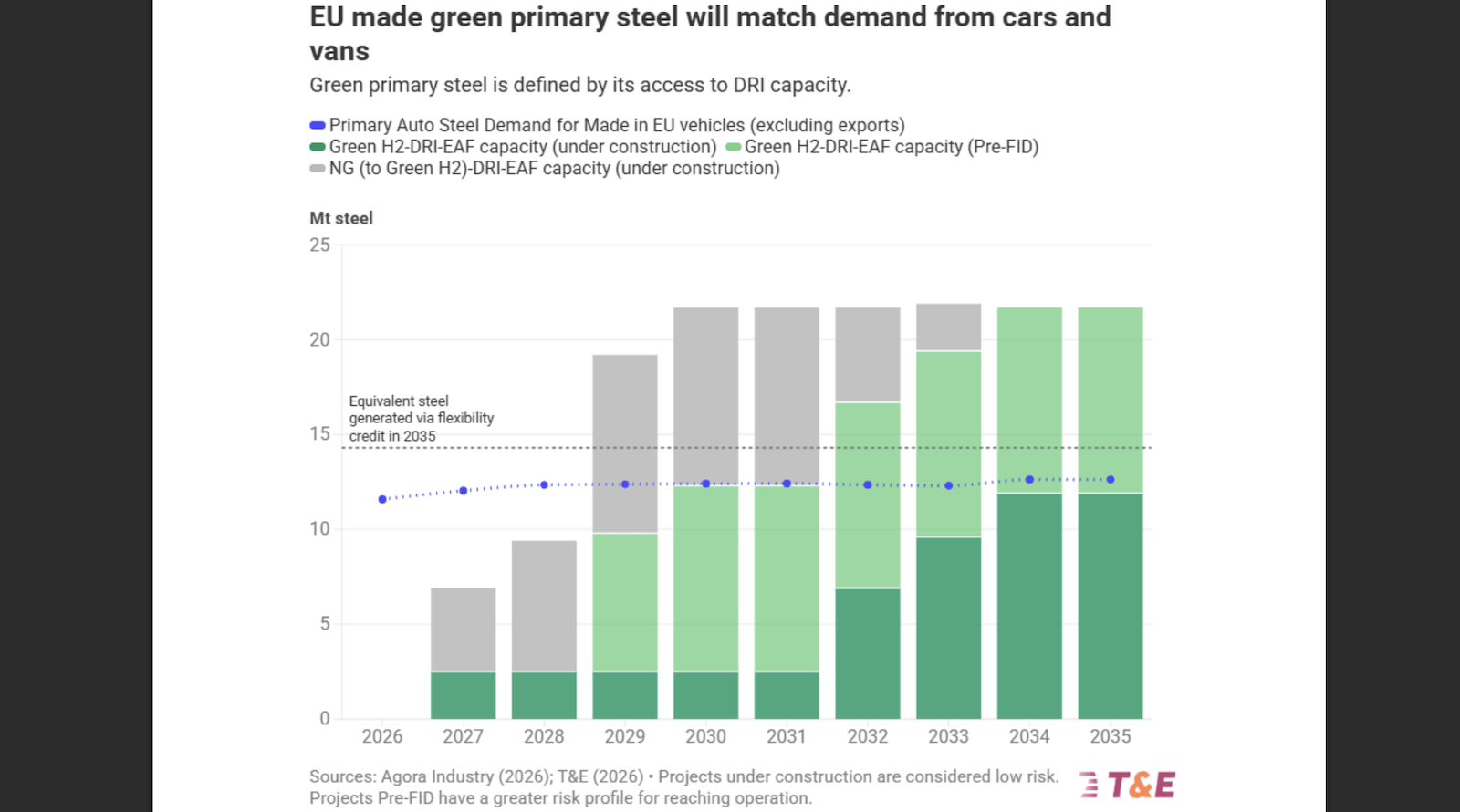

The timing could work. Modelling shows that by 2030, Europe will have enough low-carbon steel available to cover most of the automotive sector's demand. The supply is coming. The question now is whether policy can steer that supply toward genuine decarbonisation, rather than allowing it to chase accounting loopholes. If done right, Europe's cars become cleaner, its steel industry becomes greener, and the world watches a continent turn climate necessity into industrial advantage.