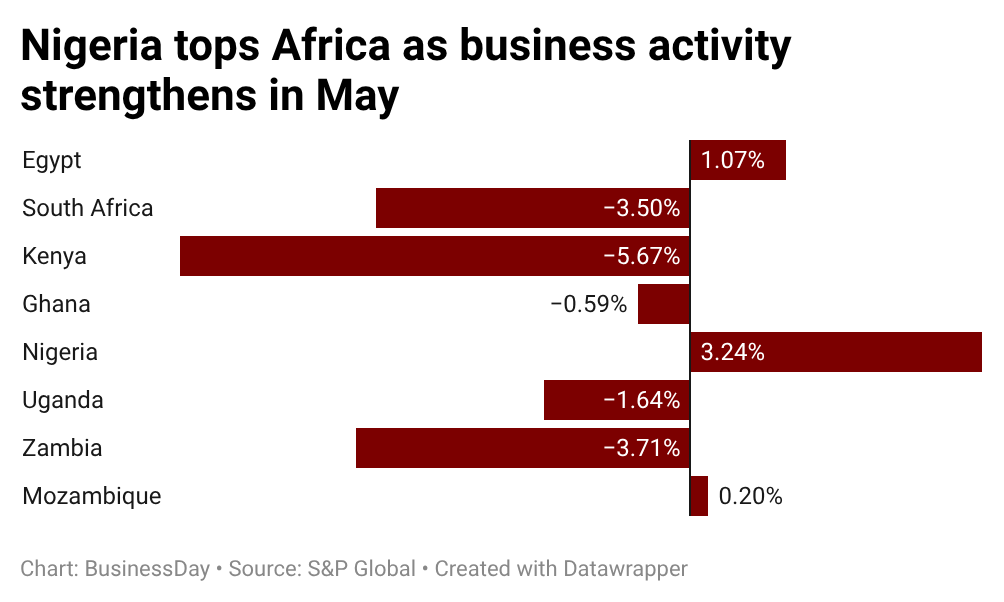

Nigeria's private sector surged past every other economy on the African continent in May, posting the region's strongest business growth even as inflation pressures mounted across the globe. The Purchasing Managers' Index—a measure of private-sector health compiled from responses by around 400 companies across agriculture, mining, manufacturing, construction, and services—jumped 3.24 percent to 54.1, the highest reading Nigeria has achieved since April 2025.

The leap matters because it signals economic resilience amid turbulence. A PMI reading above 50 points to expanding business conditions, while anything below signals contraction. Nigeria's ascent came as regional momentum weakened, with five of the eight major African economies tracked by S&P Global sliding into contraction in May—a sharp reversal from just three the month before. In this fraught landscape, Nigeria's expansion stands out.

The surge was driven by accelerated growth in both output and new orders. Output expanded at its fastest pace in seven months, while new orders grew at their quickest clip in nine months, according to S&P Global's analysis. Muyiwa Oni, head of Equity Research West Africa at Stanbic IBTC Bank, attributed the momentum to improving customer demand and new product launches. Importantly, output growth was recorded across all four broad sectors covered by the survey—a rare feat of breadth in a region grappling with uneven pressures.

Nigeria's rise carries particular weight given the competitive regional landscape. In April, Kenya had claimed the crown of Africa's fastest PMI improvement. But East Africa's biggest economy stumbled badly in May, with its PMI falling to 46.6—its lowest level in ten months—amid a resurgence in inflation and disruptions from nationwide transportation protests. Kenya's consumer inflation accelerated to 6.7 percent from 5.6 percent in April, reaching its highest level since January 2024. Nigeria, meanwhile, has now expanded for four consecutive months and reclaimed the continent's top position, which it last held in October 2025.

The achievement is all the more striking given the headwinds battering the global economy. Escalating tensions involving the United States, Israel, and Iran have roiled commodity markets over the past three months, raising concerns about disruptions through the Strait of Hormuz—a critical corridor for global oil trade. The resulting surge in energy, fuel, and fertiliser prices has begun filtering through to African economies, threatening inflation-control gains and broader food security. Input prices in Nigeria did continue to rise, though the pace of increase slowed for a second consecutive month. Output prices climbed more steeply, particularly in manufacturing and agriculture.

The World Bank has warned that Middle East tensions could have far-reaching implications for the continent, with rising fuel and food import costs potentially forcing central banks in oil-importing economies to delay interest-rate cuts. Yet Nigeria's private sector is pushing forward anyway. The trajectory suggests that despite mounting external shocks, businesses across Africa's most populous nation are finding ways to expand, invest in new products, and serve growing customer demand. Whether that momentum can be sustained as global pressures intensify remains an open question—but for now, Nigeria is the continent's growth story.