Worldsteel's latest figures cut through the hydrogen hype: the world produced 1.88 billion metric tons of crude steel in 2024, generating 2.18 tons of CO₂ equivalent per ton of steel produced. That scale makes steel one of the planet's largest industrial emissions problems—not a marginal concern, but one of the big pieces of the climate challenge that matters.

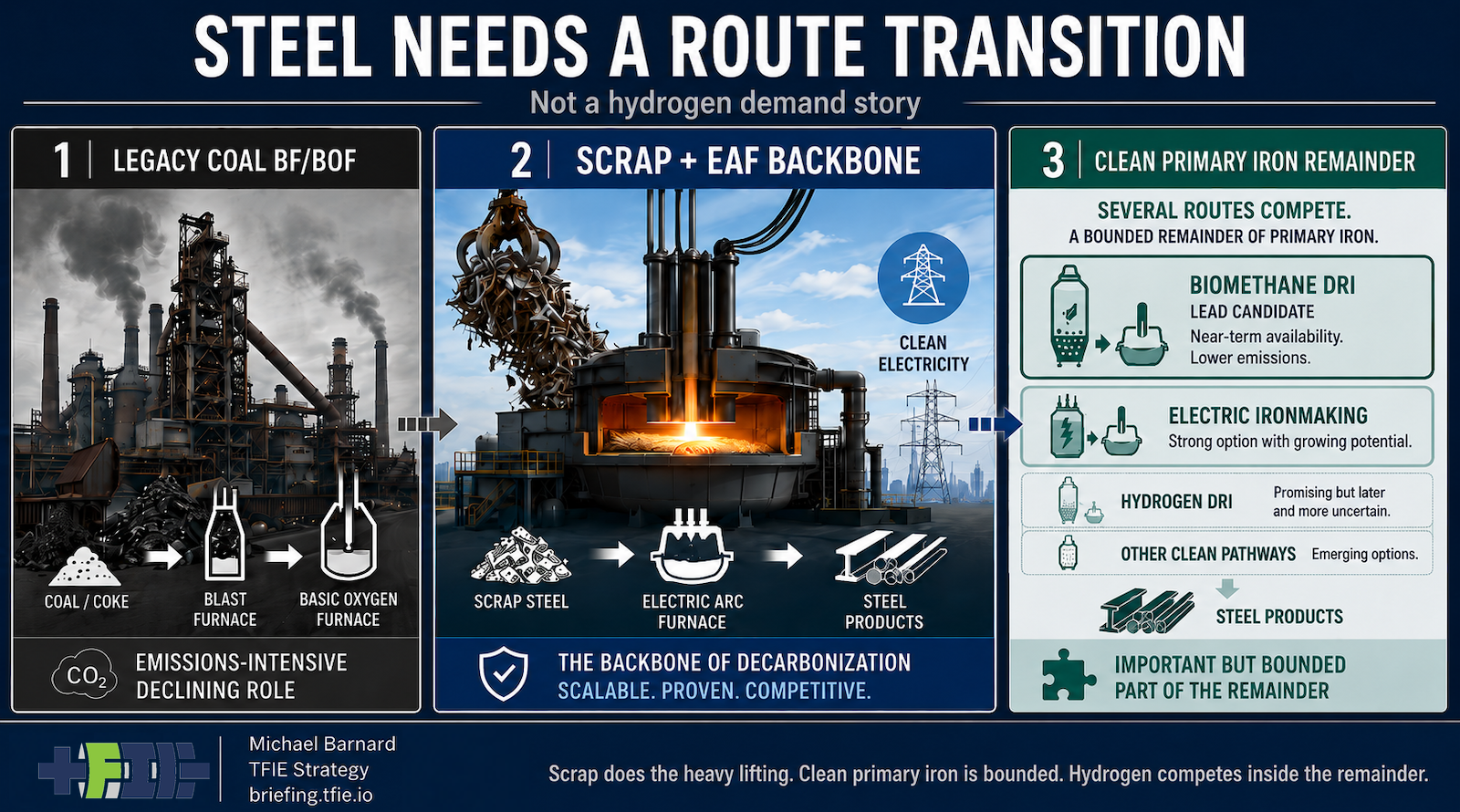

And yet the conversation keeps getting pulled in the wrong direction. Steel decarbonization keeps being framed as a hydrogen story, inviting endless discussion of electrolyzers, pipelines, storage caverns, and industrial-policy speeches hunting for customers. But steel is not a fuel. It does not disappear when used. Instead, it accumulates in buildings, bridges, ports, rail vehicles, ships, appliances, and transmission towers—then returns as scrap when those assets eventually retire. That stock-and-flow reality should be the starting point for any serious steel transition.

The real question is not how much hydrogen the sector might absorb if hydrogen were cheap and abundant. The useful questions are how much steel the world actually needs, how much can come from scrap, how much clean primary iron remains necessary, and which production routes can deliver it under genuine constraints. That framing treats steel decarbonization as a route shift, not as a hydrogen-demand forecast.

Scrap-fed electric arc furnaces are the workhorses of that transition. They are not speculative climate hardware—they are mature industrial equipment already making a substantial share of global steel wherever scrap streams, electricity systems, and product requirements align. As steel accumulates in the built environment and older assets retire over decades, the available scrap pool grows. Scrap-fed EAF production is not magic. Steel must be collected, sorted, cleaned, and matched to product specifications. Alloy contamination matters. Furnace utilization matters. Clean electricity matters. But in mature economies especially, the long-term backbone of lower-carbon steel is recycled steel in electric furnaces, not a universal pivot to hydrogen.

Clean primary iron does remain a large industrial category—it simply cannot be the entire steel system. Developing economies still need net additions to steel stock. Some steel grades require chemistry tighter than scrap can reliably provide because buildings and bridges do not retire on command. But here is where much hydrogen-for-steel analysis goes wrong: hydrogen direct reduced iron is one possible route to clean primary iron, not the definition of it. Other approaches are being tested, including more direct use of electricity, different reduction pathways, and trade in green iron units from regions with better ore, renewable electricity, port access, and industrial space. Once the clean-primary-iron category is properly bounded, hydrogen has to compete against real alternatives rather than claim the entire category by assumption.

The unsexy move that matters most is the one getting the least attention: retiring the legacy blast furnace and basic oxygen furnace route. A serious steel transition requires coal-based capacity to actually leave the system, not merely be surrounded by optimistic hydrogen announcements. That is a hard capital-stock problem. But it is the pivot that moves the needle on emissions.