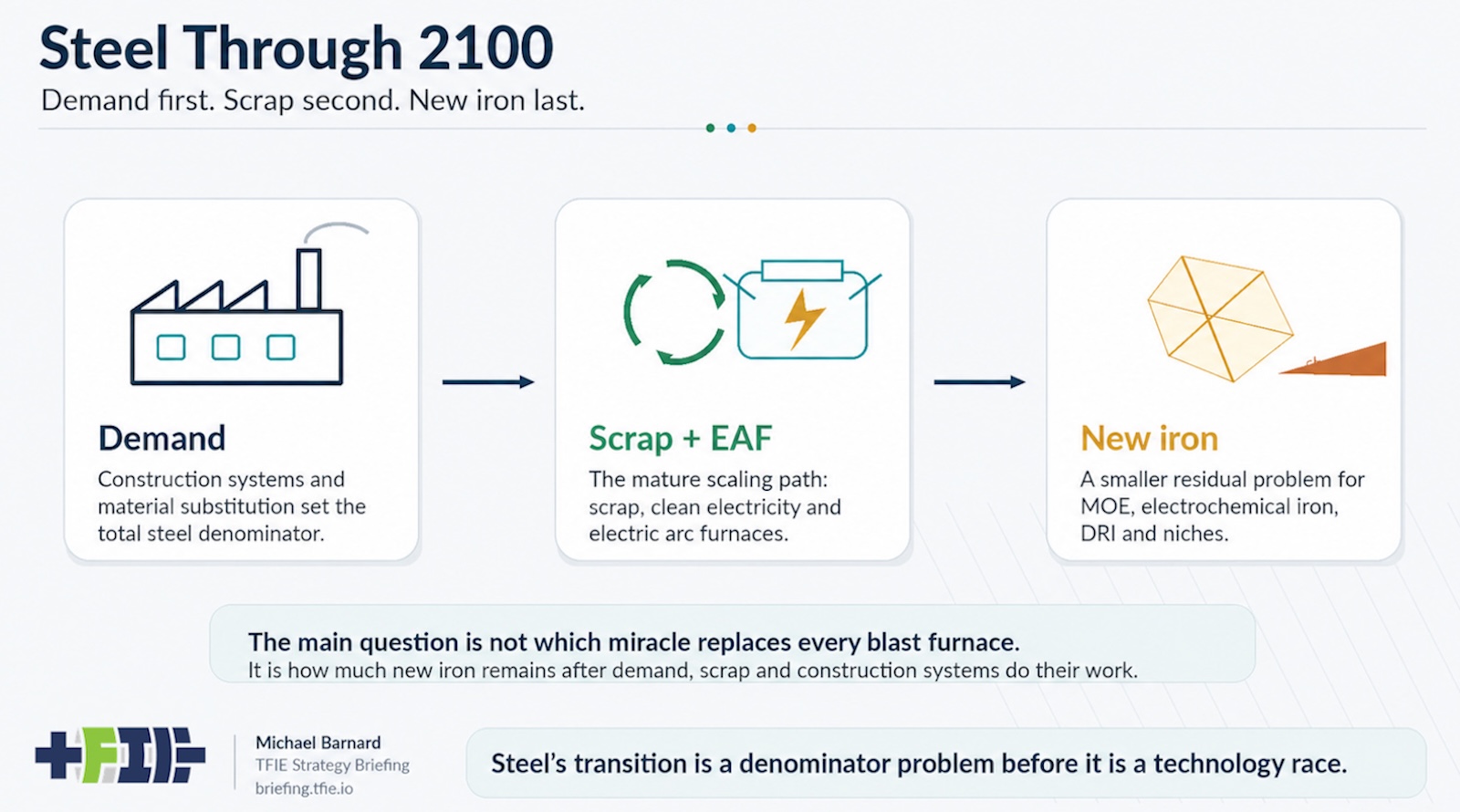

Steel has a decarbonization problem that gets the wrong solution in almost every policy briefing room. The world makes roughly 1.9 billion tons of crude steel annually, and most of it still emerges from blast furnaces and basic oxygen furnaces burning coal and iron ore—a process that produces outsized carbon emissions. But the transition toward cleaner steel won't be won by finding a single hero technology to replace every furnace. It will be won through a much more unglamorous pathway: asking how much steel the world actually needs, how much old steel returns as scrap, and how quickly electric arc furnaces can expand to meet demand.

Hydrogen has captured the imagination of governments, incumbent steel producers, and electrolyzer vendors because it offers a seductive story—replace coal with hydrogen, keep making new iron, plug it into existing infrastructure, and declare victory. The trouble is that story gets the order of the transition entirely wrong. Steel's decarbonization starts with the denominator: the material-flow problem that comes before any technology fix. That means confronting construction practices, the eventual lifespan and return of steel products, the role of competing materials like mass timber, and only then asking what role hydrogen might play in the smaller residual problem that remains.

Consider what China revealed about the scale of future demand. Its construction surge from roughly 2000 to 2020 was one of the largest material-demand events in human history—a shock of cement, steel, and urbanization that cannot simply be extrapolated elsewhere. India, Southeast Asia, Africa, and other growth regions will certainly build extensively, but assuming they will reproduce China's exact mix of steel intensity, cement intensity, and infrastructure buildout underestimates how different regional pathways can be. Lower concrete intensity in buildings changes steel demand too. The coupling between steel and cement through construction means that architectural choices—including the shift toward mass timber and cross-laminated timber construction—make some future steel demand less inevitable.

Scrap is the structural correction that transforms the entire equation. Steel is not a fuel that vanishes after use; it is a long-lived material that eventually returns from buildings, vehicles, machinery, infrastructure, appliances, and industrial systems. Quality issues exist, and certain products require cleaner metallic inputs than mixed scrap can provide. But a substantial portion of future steel demand will be met by steel the world has already manufactured and will recover from its current stock.

Electric arc furnaces are therefore not speculative technology or lab curiosity—they are already an industrial steelmaking route that dominates production in some markets. They can melt scrap, direct reduced iron, pig iron, and other metallic inputs using electricity, and as electrical grids decarbonize, their emissions decline proportionally. Real constraints matter: copper contamination, regional scrap availability, electricity prices, and customer qualification all present genuine challenges. But the route is mature, commercial, and scalable in ways that many emerging iron-production technologies simply are not.

This is where the green-steel narratives that dominate headlines start to fracture. A pilot program is not a market. A hydrogen direct reduced iron announcement is not a durable steelmaking strategy. Real progress appears in blast furnace retirements, electric arc furnace facilities running at high utilization rates, and the systemic shift toward a material-flow model that treats scrap recovery and demand management as the center of the solution rather than afterthoughts to hydrogen's shiny promise.