The United States now has enough clean energy capacity on the grid to power nearly 80 million homes—a milestone that underscores how far renewable electricity has come, even in uncertain times. According to the Q1 2026 Clean Power Market Report released by American Clean Power, cumulative clean energy capacity across the country has reached 370 gigawatts, a testament to the competitive economics that make renewables unstoppable regardless of political headwinds.

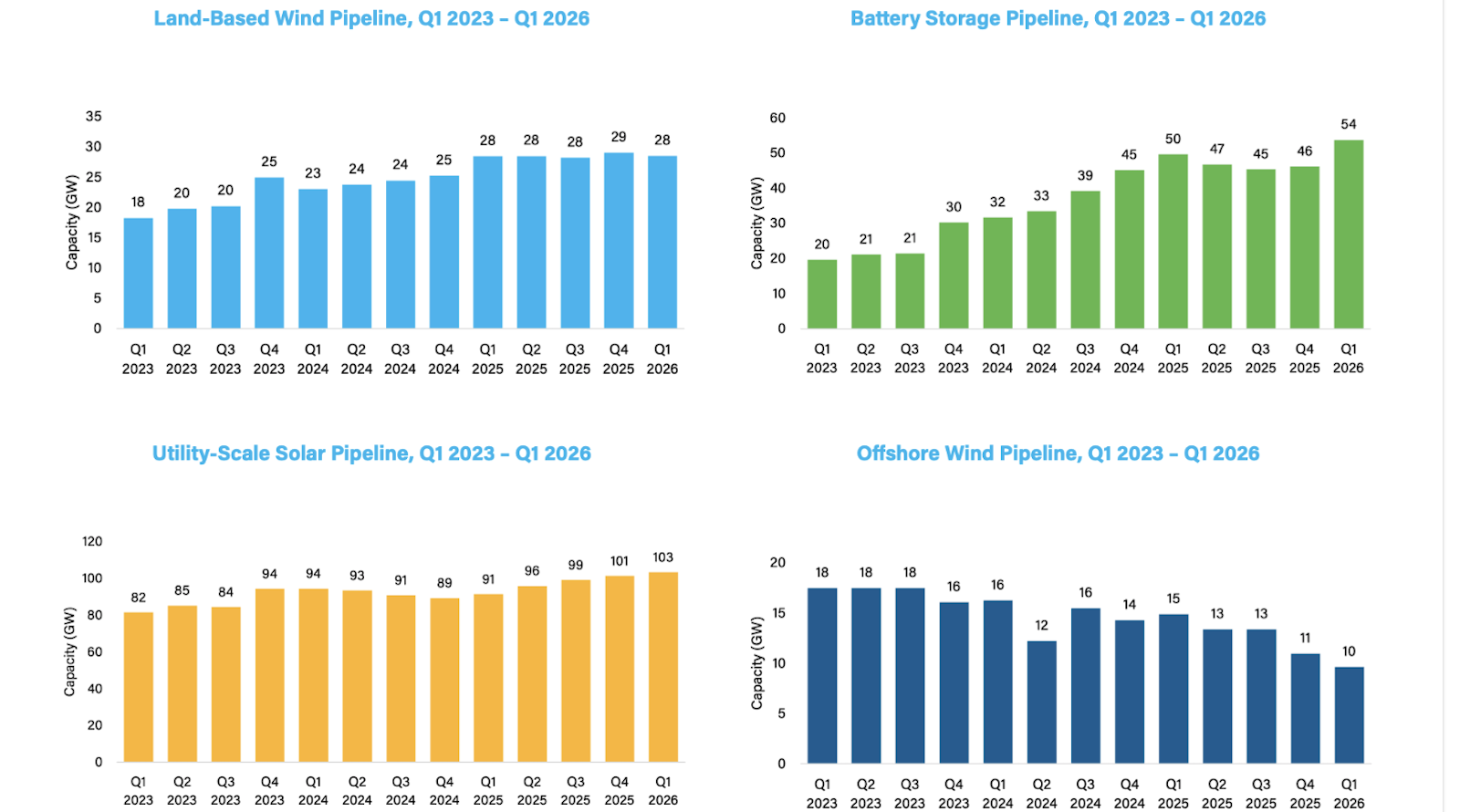

The numbers tell a story of a sector that refuses to be held back. While government support for solar has declined—even in California, the nation's top solar state—the technology has become so cost-effective that the pipeline for solar projects grew by 13% in the first quarter alone, leading all clean energy technologies. Battery storage followed with an 8% pipeline increase, fueled by its low costs and critical role in stabilizing the grid. Together, these two technologies demonstrate why utilities and developers continue betting on clean energy: the economics simply work.

Solar power added 3.6 gigawatts of capacity in Q1 2026, bringing its cumulative total to 161.1 gigawatts—enough to power nearly 600,000 American homes. The milestone is particularly significant because solar has now surpassed onshore wind as the nation's largest source of installed renewable capacity. Onshore wind, which finished the quarter at 160.9 gigawatts, remains close behind, and a substantial pipeline of wind projects is expected to come online later this year, so the lead may shift again.

Texas exemplifies the trajectory of this clean energy transformation. The state now hosts 96.4 gigawatts of installed clean power capacity—26% of the nation's total—and is on the verge of becoming the first state to reach 100 gigawatts. With 1.6 gigawatts added in the first quarter alone, Texas could hit this milestone before year's end, a remarkable achievement for a state traditionally synonymous with fossil fuels.

Yet the picture is more complex than pipeline growth alone suggests. Actual installations of clean energy capacity declined by 17% year-over-year compared to Q1 2025, falling from 7,695 megawatts to lower levels. This slowdown was largely expected, as projects approved during the Biden administration were energized in 2025, creating a natural lull in 2026. The seasonal pattern also played a role: first quarters are typically slower than fourth quarters, and Q1 2026 installations fell 66% compared to Q4 2025.

More troubling is the growing backlog of delayed projects. Over 6.4 gigawatts of clean power capacity that was originally scheduled to come online in Q1 never did, adding to a backlog of 53 gigawatts worth of stalled projects. Developers cite lengthy permitting processes, congested interconnection queues, and fluctuating equipment prices as culprits. These administrative and logistical barriers reveal where the real bottlenecks lie.

Perhaps most striking is the offshore wind sector, where the pipeline dropped 35%—a direct result of regulatory and permitting challenges compounded by the current administration's hostile stance toward the industry. Land-based wind projects also struggled to secure federal approvals. Yet despite this headwind, the overall clean power pipeline—projects in development or planning stages—surged to 195 gigawatts, representing more than half of the current installed base.

What emerges is a portrait of an industry caught between momentum and uncertainty: pipelines and capacity growing robustly, installations slowing, and permitting systems creating dangerous bottlenecks. The competition and cost dynamics that have driven renewable energy forward remain potent, but unlocking the full potential of that 195-gigawatt pipeline will require solutions to the permitting and interconnection challenges that now threaten to slow the transition.