In early December 2025, a Wrightbus hydrogen bus caught fire in Crawley, forcing Metrobus to withdraw its entire fleet of single-deck hydrogen vehicles from service as an immediate precaution. No injuries were reported, but months later the buses remain grounded—a stark reminder that the real challenge with hydrogen transit isn't technology alone, but the unglamorous work of keeping specialized fleets operational when the numbers don't yet justify the infrastructure costs.

The Crawley incident matters not because it proves hydrogen buses are inherently unsafe, but because it exposes a structural problem few transit systems want to discuss: when a hydrogen fleet is small, specialized and dependent on a thin support ecosystem, one incident cascades into service disruptions that become increasingly hard to justify. Diesel buses catch fire too. Battery-electric buses have failures. But the operational consequence is what transit agencies actually run on—vehicle availability, route reliability, maintenance capacity, fuel logistics and spare parts supply. For hydrogen, that support tail is disproportionately long when you're operating just 20 buses rather than hundreds.

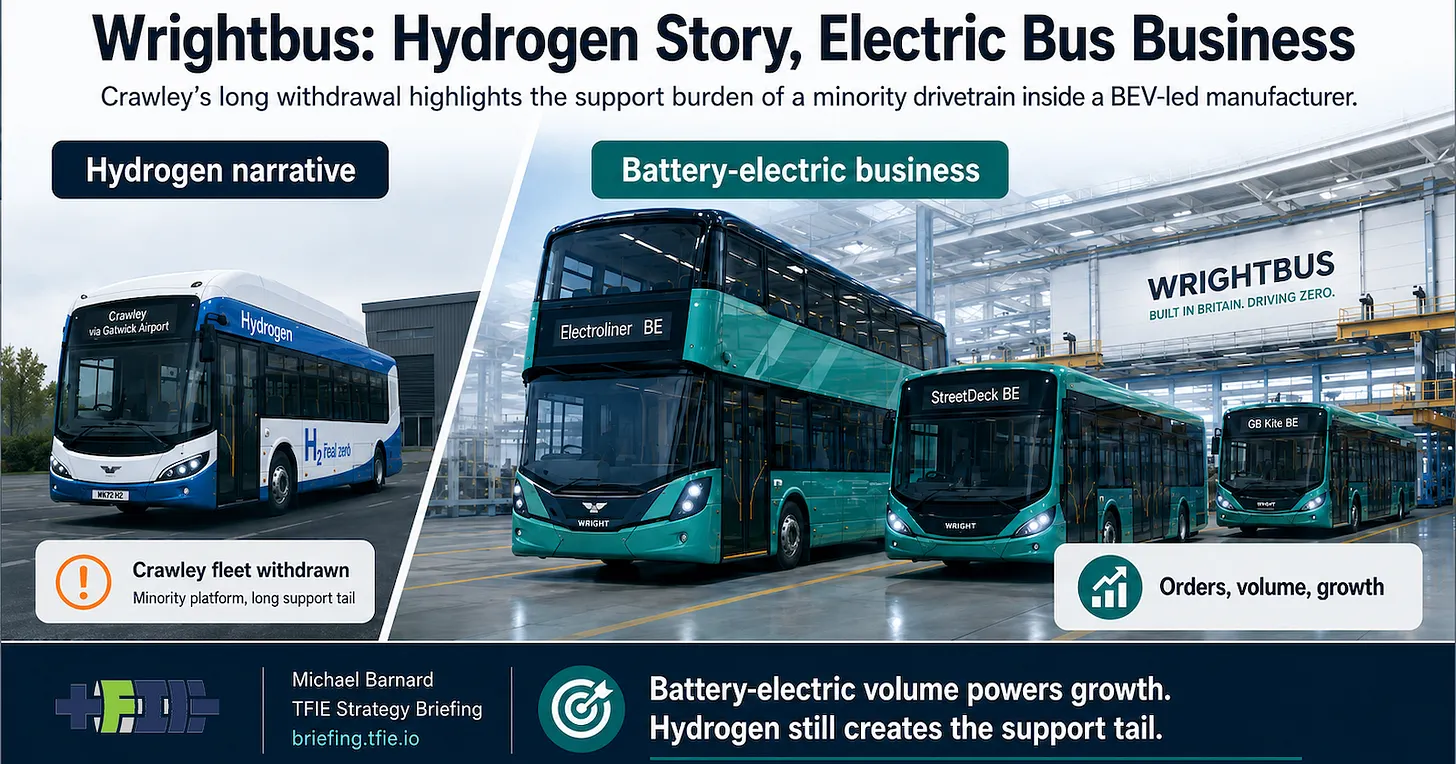

Wrightbus, the UK bus manufacturer that emerged from administration with considerable political fanfare, arrived with hydrogen as central to its recovery narrative. Hydrogen made the story legible to ministers and the press: UK-built zero-emission buses, a liquid hydrogen refuelling station, visible links to domestic manufacturing and a connection to the broader JCB hydrogen push. The Crawley project involved 20 Wrightbus GB Kite Hydroliner buses serving routes around Gatwick and Horley, with another 34 planned, positioning it well beyond a token demonstration and into genuine fleet operations. The hydrogen was stored in liquid form at the Metrobus Crawley depot, then converted to gas for use in the buses—a supply chain that worked until it didn't.

The distinction between brand architecture and commercial gravity, however, cuts straight to why hydrogen's policy narrative is increasingly diverging from manufacturing reality. Wrightbus' visible large-scale orders and momentum are decisively skewed toward battery-electric buses, particularly its Electroliner model, not hydrogen fleets. Hydrogen helped make the recovery story politically attractive and gave the company national-manufacturing credibility. But it is not carrying production volume or driving the company's scalable business model.

The support problem crystallizes this tension. A hydrogen fleet is not simply a set of buses. It demands fuel supply infrastructure, trained maintenance technicians, specialized diagnostics, emergency procedures for fire and hydrogen leaks, spare parts inventories, driver confidence building and operational workarounds when vehicles are unavailable. When hydrogen represents a minority drivetrain inside both an operator's fleet and a manufacturer's order book, that entire support structure becomes increasingly difficult to justify against the scale and standardization of battery-electric fleets.

Wrightbus will likely continue building hydrogen buses. But the scalable business is battery-electric manufacturing, and that is where the company's commercial center of gravity now sits. The Crawley fire doesn't prove hydrogen can't work—it simply makes the economic case for small hydrogen fleets, stretched across specialized infrastructure, visibly harder to defend when you're competing for resources against larger, simpler, and operationally more resilient electric bus deployments.